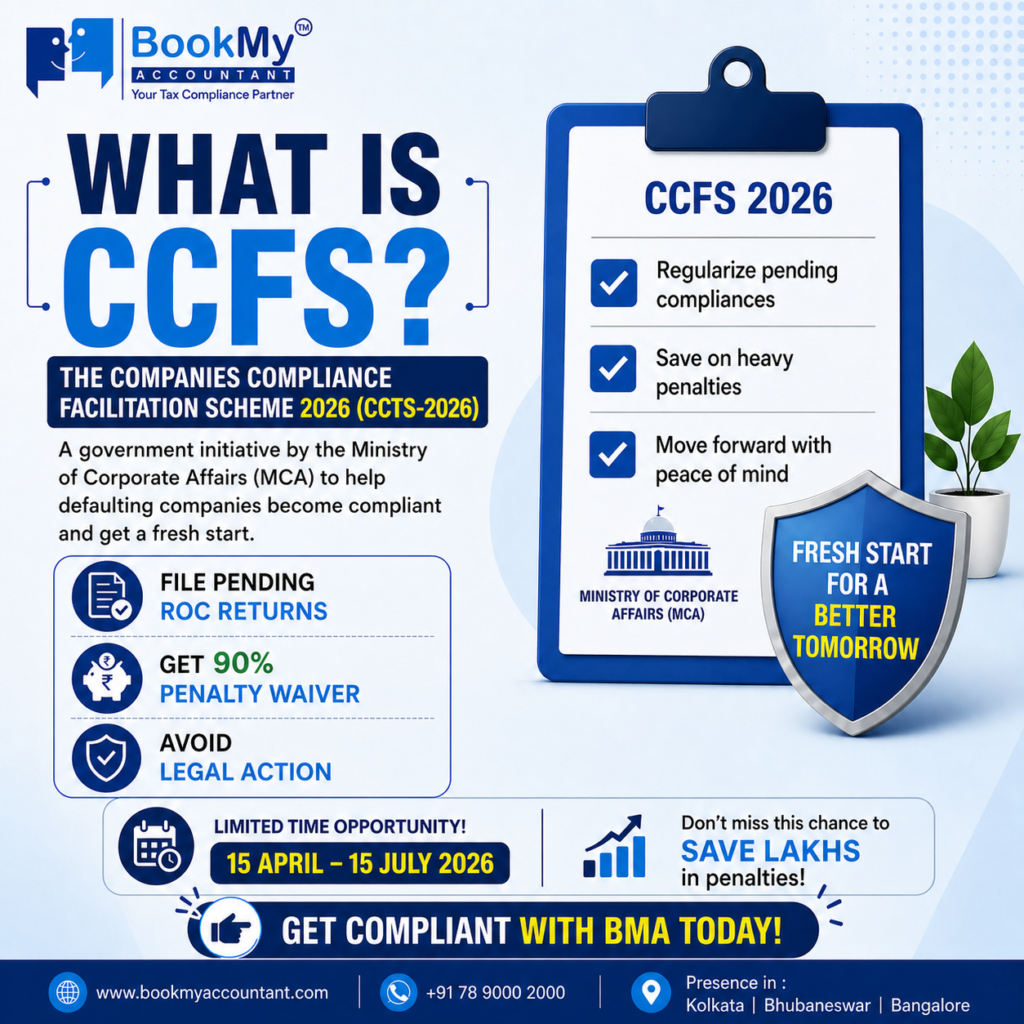

CCFS Scheme 2026: A One-Time Opportunity to clear pending ROC Filings at 90% reduced cost

In today's era, the regulatory compliance framework has become extremely important, and therefore we cannot take it casually. The CCFS Scheme 2026, also known as Companies Compliance Facilitation Scheme (CCFS-2026) is the golden opportunity for Indian companies to regularise the pending filings and to improve compliance position in order to avail the benefit of significant reduction in additional fees and penalties.

Owing to high searches over compliance relief, penalty waivers and ROC filings, the CCFS Scheme has immediately grabbed attention for those companies wanting to get themselves out of further risks.

CCFS Scheme Explained

CCFS Scheme is designed to offer a compliance relief by facilitating the companies having pending statutory compliances to update its status within the specified period of time. This system offers a structured route for the non-compliant companies to achieve compliance in less possible financial risks.

Under the CCFS Scheme, the defaulting company can file its pending documents by way of reduction of penalties so as to remain compliant and reduce regulatory risks.

Why CCFS Scheme is so important in 2026

The importance of the CCFS Scheme in 2026 is driven by the following three factors:

Strict Compliance Under MCA: The concerned authorities are monitoring all compliances.

High penalties if you are not compliant: In case of defaults, companies can land in to huge financial liabilities.

Limited period for the relief: This is a one-time relief period offered to correct compliances.

For many businesses, this is not a mere compliance but a way for survival and future credibility.

Key features of the CCFS Scheme

There are a lot of benefits under the CCFS Scheme, some of them being:

Significant reduction in additional fees (up to 90% waiver)

Companies can file the pending documents with minimal additional fees.

Regularise pending compliances

Companies will have to update all the pending records.

Immunity from penalties and prosecution, subject to prescribed conditions under the scheme.

Eligible companies may also opt for dormant status or apply for strike-off at reduced compliance cost under the scheme.

This scheme reduces the chances of authorities charging you under any relevant section with penal provisions.

Cover for all pending filings

These are some of the critical filings:

AOC-4

MGT-7

Director KYC compliances.

Who can benefit from the CCFS Scheme

Every company with any pending ROC filings that is marked as non-compliant with MCA would benefit from the scheme. But, the company that is undergoing any liquidation proceedings and is under some special law or under a regulatory procedure is not covered under the scheme.

Timeline for the CCFS Scheme

15 April 2026 - 15 July 2026

Companies should surely keep an eye on these dates for the smooth compliance process.

Process for Availing CCFS Scheme

The steps to comply under the CCFS Scheme are:

Get yourself to the compliances; Review each of your pending compliances on the MCA website.

Get the necessary documents: Collect your financial statement, Board's report etc and keep them ready for filing.

Get it filed: Submit the forms i.e. AOC-4 or MGT-7 to the respective RoC and pay only the statutory fees as prescribed under the scheme.

Compliances achieved: All your compliances are now done.

Business Benefits

Companies are provided with the following benefits while using the CCFS Scheme:

Cost-effectiveness

Reduction of penalties and additional fees

Regulatory support.

Credibility and reliability: improve faith in investors.

Seamless operations

Risk if we do not take this opportunity

Failure to utilise the scheme may result in heavy additional fees, penalties, potential prosecution, director disqualification, possible strike-off of the company, and increased regulatory scrutiny by MCA. If an organization doesn't capitalize this opportunity then it might end up spending much more on legal compliances and penalties in the future.

How BMA Can Help You.

BMA is known for the end-to-end services offered for the compliances. Book my Accountant can provide you assistance and can act as a partner in all your regulatory requirements and compliance filings, so that you get the optimum benefits out of the CCFS Scheme and further focus on expanding your business growth.

Conclusion

The CCFS Scheme 2026 is an invaluable opportunity that provides companies with a much-needed relief to correct past defaults in compliances without significant financial impact and strengthen future regulatory position. As regulatory scrutiny continues to grow, acting promptly and utilizing this scheme will be crucial for businesses to maintain credibility, avoid legal repercussions, and ensure sustained operational success. It is highly recommended for all companies to thoroughly assess their current compliance standing and take the necessary steps within the designated timeframe to make the most of this important initiative. The relief under the scheme is primarily applicable to additional filing fees, and immunity from penalties or prosecution is subject to compliance with scheme conditions and applicable provisions of law

Disclaimer

This article is solely for informational and general guidance purposes only. The information provided is based on our understanding of the current regulatory provisions as on the date of writing this article and may be subject to change without any prior notice. No portion of this content shall be considered as legal or professional advice. The Author and the publisher take no responsibility or assume any liability for any actions taken in reliance upon the information in this article.

Income Tax Act 2025: Myth vs Reality on Privacy & Digital Access

Introduction: Keeping Fear off Facts.

The suggested Income Tax Act 2025 has caused a commotion among taxpayers, entrepreneurs, and specialists. There has been a sense of constant dread at boardrooms and client meetings: Am I now afraid that tax officers now have access to my personal photos, videos, and WhatsApp chats?

The fear is actual. In the current digital era, we live in virtual space in most aspects of our personal and financial lives. But the law as perceived has been ahead of what the law is.

Important Implication: The majority of fears regarding the Income Tax Act 2025 are fallacies. The basic protection mechanisms are present.

Is This Really New? Learning about the Current Powers held by Tax Officers.

The History of Tax Investigative Authority.

The Income Tax Department has not been functioning without investigative authority. Tax officers have wide rights to:

Carry out search and seizure operations.

Calling for information and records.

Look at instances where the income has evaded measurement.

Access undisclosed assets

These powers have changed with the economic and technological developments.

The Digital Records Revolutionized It all.

The move towards the digital records as opposed to the hardcopy books did not spare the tax law. Key developments include:

Court Acceptance of Digital Evidence:

Digital files, accounting software, and emails are now regarded as documents.

The cases in which electronic records are reviewed are not new in tax cases.

The use of cloud storage and digital devices has been examined in the proper cases.

What This Means: It is not a new practice that tax investigations are accessing digital data, as this has been occurring since a long time.

The Fundamental Protection: "Reason to Believe"

Protecting Your Privacy What.

The most important legal prerequisite in any tax investigation is the requirement that there be a reason to believe that:

Income has been hidden.

There is evidence of tax evasion.

There are undisclosed assets.

This is not just a formality. This has been highlighted in a variety of cases as a substantive protection.

No "Fishing Expeditions" Allowed

Tax officers are not allowed to make random searches in the hope of discovering something. Investigations must be:

Supported by reliable facts.

Guided to unearth certain financial wrongs.

In accordance with the suspected violation.

The Principle of Relevance: Legal Limit of Your Privacy.

What Data Are Analysable?

The legislation does not allow the random access to all information on the seized devices. The area of investigation directly correlates with the purpose of investigation.

Information that is illegally subject to examination:

Unrelated to income or assets, personal photographs.

No financial connection family videos.

Personal messages which have no financial implications.

Privacy: Essential Constitutional Right.

Privacy has become a constitutional right in India. This serves as a constitutional limitation that investigative agencies should not infringe.

Key Rule: Although data may be stored in a device, it is not subject to a legal search unless that information is somehow related to the financial status of the taxpayer.

What is in Real Time Changing: The sense of Virtual Digital Space.

The Real News About Income Tax Act 2025.

The new concept that is pointed to by the proposed framework is the virtual digital space.

This does not add any new powers- it only defines old ones.

Why This Matters

Data storage today is radically different:

Information is not only on physical devices but it also exists in the cloud.

Data is distributed in several servers.

Online accounts are accessed and not stored on-site.

Past Situation: The officers were able to access such data but had problems with interpretation.

New Framework: It is stated in the law that when the information in digital and remote data repositories is financially relevant, they may be reviewed.

The Principle behind the Underlying is the same.

Relevance is still the determining factor. The fact that data is available does not imply that it could be legally examined.

Digital Forensics: Technology vs. Legal Authority.

The Modern Investigation Tools with What They Can Do.

Modern methods of digital forensics have enabled the officers to:

Recover deleted files

Analyse metadata

Trace transaction trails

Restructure financial operations accurately.

The Critical Distinction

A very important distinction lies between:

Accessibility to Data = Technologically improved.

Permission to Use Data = Still subject to the law.

Technology enhances the effectiveness of enforcement, but does not increase the scope of the law. Relevance, necessity, and proportionality are still in force.

The Check of Overreach by the Judiciary.

Courts Protect Taxpayers

The Indian courts have always served as a protection:

When searches are unreasonable or unwarranted, courts come in to play.

Prohibitions on arbitrary or disproportionate action apply no less in the online environment.

The higher degree of digitization can provoke a greater court control as sensitive personal information is being used.

Your Legal Remedies

Taxpayers cannot be powerless. Any abuse to investigative powers can be contested by:

Writ petitions

Pursuing the higher tax authorities.

Court interventions

When Pictures and Videos become Relevant.

The situations that are under investigation.

In such cases, visual evidence can legitimately be a part of the investigations:

The undisclosed assets are owned by the company.

Images or videos of valuable property that is not mentioned in returns.

2. High-Value Transactions

Graphical record of major financial transactions.

3. Lifestyle Inconsistency

Track record of a lifestyle that is extreme to what is claimed to be earned.

The use of social media that displays unaccounted wealth.

The Key Distinction

The analysis is done on its evidentiary value, rather than its personal nature. Law is about income, property, and observance, not spying on personal life.

What This Implicates to Obedient Taxpayers.

The Movement towards Transparency.

The digital ecosystem brings more transparency and accountability, as opposed to surveillance.

Through transactions, communications and social media, your online history can be used to:

Corroborate financial information

Detect inconsistencies between stated and real income.

Verify consistency in financial reporting

What You Need to Know.

This doesn't mean:

All posts will be investigated.

Messages in private are automatically screened.

The access of tax officers is unlimited.

It does mean:

Discrepancies in stated income and indicators of visible wealth might be of interest.

The conventional differences between disclosed and actual financial positions are more difficult to conceal.

The environment is moving towards becoming data-driven.

Guidance of Professionals and Taxpayers.

In the case of Chartered Accountants & Tax Advisors.

Change the discussion on fear to readiness.

Focus clients on:

Proper Documentation

Keep good organized financial records.

Keep supporting documentation for all transactions

Accurate Reporting

Disclose all income and be honest.

Make sure that there is uniformity in all filings.

Digital Hygiene

Maintain clear records

Avoid informal arrangements

Make sure that there is consistency in financial and non-financial data.

Substantiation

Store receipts and invoices to all claims.

Shun dealings unexplainable.

For Individual Taxpayers

Practical Steps:

✓ Maintain a tidy financial record.

✓ Report all sources of income

✓ Maintain transaction documentation

✓ Check that your lifestyle is in line with stated income.

✓ Do not use informal or cash transactions.

✓ maintain records of major purchases.

The Most Widely known misconceptions of the Income Tax Act 2025.

Myth 1: "Tax officers can now access my personal photos"

Reality: They are not able to view any other photos but those related to your monetary matters. Personal images that have nothing to do with income or possessions are not exposed.

Myth 2: "The law is an infringement of privacy altogether.

Reality: Constitutional rights to privacy and principles of relevance under the law remain. Protective measures have not been removed.

Myth 3: "This is totally new power.

Fact: There have been years of digital access. The 2025 law is not the expansion of authority.

Myth 4: "no one can prevent the government excesses.

Reality: Courts are proactive in interfering with overreaching searches. The misuse can be contested in a legal manner.

The Law Framework Continues to defend you.

Values That Stand the Test of Time.

These defences persist, in spite of technological progress:

"Reason to Believe" Requirement

When carrying out investigations, credible information has to be used.

Random searches are prohibited.

Relevance Doctrine

Information has to be connected with finances.

The privacy of personal information is maintained.

Privacy Rights

Fundamental constitutional protection

Provides a limit to investigative power.

Judicial Review

Excessive searches can be reversed by the courts.

Proportionality standards apply

The Bottom Line: What Is Really Changing in What Income Tax Act 2025.

What's Different

Categorical identification of virtual digital space.

Easier terms on cloud and remote data.

Recognition of contemporary storage techniques.

Greater technological investigation ability.

What Has Always Been.

Basic protection against caprice.

The constitutional right to privacy.

Conditional requirement of reason to believe.

Principle of relevance

Judicial oversight

For Compliant Taxpayers

There is nothing to be afraid of.

The changes are indicative of a shift towards:

Greater transparency

Technology-driven administration

Better financial reporting.

Even-playing field among compliant businesses.

Summary: The Best Protection is Information.

The belief that Income Tax Act 2025 will allow unfettered, general access to private digital content is a major fallacy.

The basic principles of investigation are unchanged:

Reason to believe

Relevance

Respect for privacy

What's Truly Changing

It is not the legal boundaries that are so clear, but rather the ease with which digital spaces are introduced into the legal framework, and the advanced tools that the authorities can use.

Moving Forward

To professionals and taxpayers that comply with taxes:

Know the law and not be afraid of it.

Maintain proper documentation

Be honest and frequent in the reporting.

Understand that digital hygiene is important.

The introduction of the Income Tax Act 2025 is not something to panic about, but instead an indication that the administration of tax is becoming more open and more technology-focused.

Uncertainty is best countered by informed knowledge. The professionals are expected to offer direction to the clients in a clear, balanced, and confident way.

Key Takeaways Summary

Aspect

What's Changed

What Remains

Digital Access

Now explicitly stated

Still requires relevance

Data Types

Cloud & remote data recognized

Privacy protections intact

Investigation Tools

More sophisticated forensics

Legal standards unchanged

Taxpayer Protection

Clearer boundaries

Judicial review available

Frequently Asked Questions: Your Vote Matters.

Q1: Is it possible that tax officers can examine my personal photos?

A: Yes, only when they are pertinent to your financial matters. The personal pictures that do not refer to income or assets cannot be legally searched.

Q2 : Can authorities find my WhatsApp private even after they take my phone?

A: Yes, except in case of messages that have evidence of the financial transactions or unreported income. Conversations made privately are guarded.

Q3 : Should I panic over the changes made in 2025?

A: No. Obedient taxpayers need not be afraid, but report and record correctly.

Q4 : Are random searches permitted by the officers?

A: No. They must have a reason to believe that there is evaded taxation. No fishing expeditions are allowed.

Q5 : What shall I do to keep safe?

A: Keep good records, disclose income correctly, do not transact informally and be consistent in your reporting.

Conclusion: Navigate the Future of Taxation with BMA

The Income Tax Act 2025 is designed to modernize India's tax framework, not to invade your privacy. By separating the myths from the realities of digital access, we've aimed to provide clarity and peace of mind. The key lies in understanding the provisions and ensuring diligent compliance.

Don't let uncertainty about digital access or privacy concerns cloud your financial future.

Ready to ensure seamless compliance and complete peace of mind?Contact BMA today for expert guidance on the Income Tax Act 2025 and beyond!

Disclaimer

This website is intended to provide information and education (in general) to the reader and should not be regarded as advice on any issue, including legal advice, tax advice, or compliance advice. Legal requirements, notifications and tax laws may change. Readers should seek professional advice from a qualified professional for a thorough understanding of their own situation or check the latest legal amendments on the government websites. Book My Accountant (BMA) provides professional services; however, this document's content is not intended to be a substitute for BMA's personal advisory services.

A Guide to Section 43B(h) of the Income Tax Act, 1961 - MSME Payment Policy

The tax compliance world in India has changed significantly due to the mandatory requirements introduced under Section 43B(h) MSME Compliance of the Income Tax Act, 1961, as amended from time to time. Effective from 1st April 2024 (AY 2024-25), this regulation has created a major shift in how businesses must handle payments to Micro and Small Enterprises registered under the MSMED Act.

This guide has been designed to help Business Owners, Accountants, CFOs and Compliance Officers understand what Section 43B(h) entails, why timely MSME payments are now critical, and how to implement full compliance in a practical and user-friendly manner.

Significance of Section 43B(h) for Your Organisation

The purpose of Section 43B(h) of the Income Tax Act 1961 has been to create the following positive outcomes for businesses based in India:

To support large-scale companies in making timely payments to their MSME suppliers or providers of services,

To increase cash flow for MSMEs that supply products and/or services by enabling them to generate working capital through improved turnover,

To hold large-scale companies accountable for their ability to make timely payments to MSMEs,

To limit the flexibility of large-scale companies' ability to claim tax benefits based on their timely payments to MSMEs.

Under the provisions of this section, any expense claimed by a business for tax deduction cannot be allowed if any payment(s) made by that business to MSMEs occur later than the specified time limits of 15 days or 45 days from the date specified in either a written or oral agreement. Importantly, if you have been able to deduct a particular expense for tax purposes because you have made a payment on the day you incurred it, the only way you can deduct it subsequently is if you... have made a payment within the time specified for your deduction.

Classification of MSMEs According to the MSMED Act

Section 43B(h) only applies to those suppliers whose registration as Micro or Small enterprises was through Udyam Registration.

MSME Classification According to the MSMED Act 2006

Classification of Enterprise

Investment Threshold

Annual Turnover Threshold

Micro Enterprises

≤ ₹1 Crore

≤ ₹5 Crore

Small Enterprises

≤ ₹10 Crore

≤ ₹50 Crore

🔹 Medium Enterprises are not included under Section 43B(h).

🔹 Retailers and wholesale suppliers will also not qualify to claim the benefits under Section 43B(h), even if they hold a Udyam Registration.

Legal Framework: Section 15 of the MSMED Act in conjunction with Section 43B(h) of the Income Tax Act

Section 43B (h) relies on the definition of legally permitted times for payment as set forth in Section 15 (MSMED Act 2006).

3.1 Timelines for Payments under Section 15 of the MSMED Act (2006).

a. The Payment Terms of an Agreement (maximum 45 days) Buyers and suppliers agree to mutually-set payment terms of the agreement cannot be longer than forty-five (45) days.

Consequently, neither MSME contracts may require payments within sixty (60) or ninety (90) days of acceptance/delivery.

b. If no written agreement is present, the payment should occur no later than fifteen days from the date of the acceptance, or delivery of the items/services.

What is the Day of Acceptance? The day on which the items or services were delivered. If the buyer has any issues or concerns regarding the Delivery and they raise the matter in writing within fifteen days of acceptance/delivery, the date when the buyer resolves their issue or concern is considered "the day of acceptance".

3.2 The tax effects of section 43B(h)

Expenses (i.e. A deductible expense) : Where payments made within the 15 to 45 days of the due date (including any portion before the due date), the financial year of the payments shall be deemed to be the year of the deduction.

Non-Expenses (i.e. Not a deductible expense): Where payments made after the 15 to 45 days of the due date, the financial year of the payments shall be deemed to be the year of the payment. You cannot utilize payments prior to the filing of your tax return as per the provisions of section 43B of the Income Tax Act.

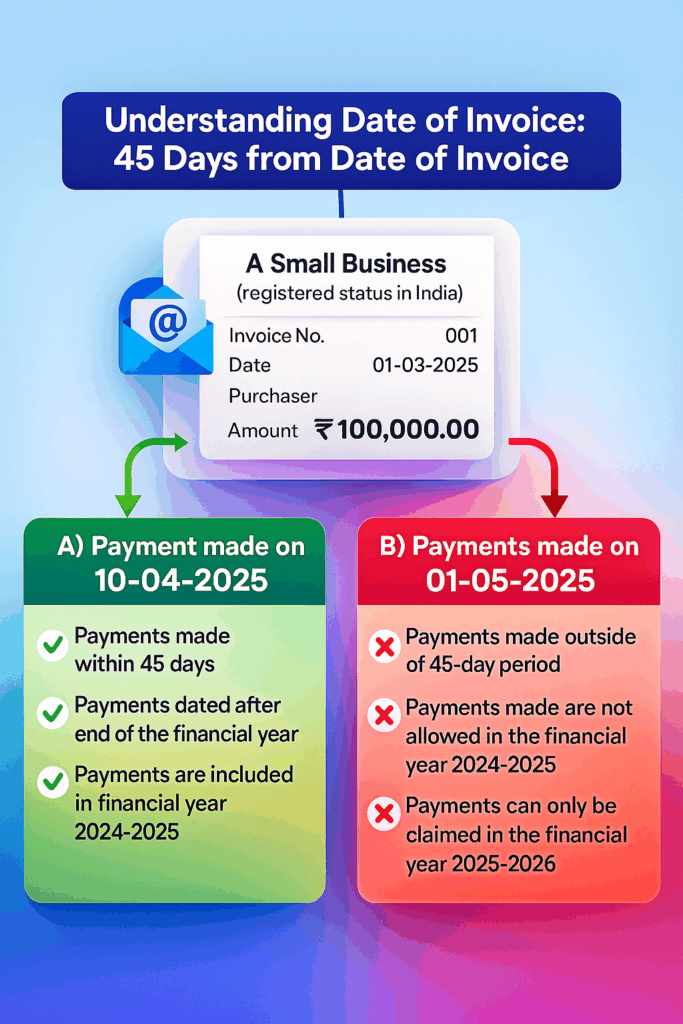

An Example to Illustrate

An electronic invoice is sent to a Purchaser on 01-03-2025

Seller Name: A Small Business (with a registered status in India) Understanding Date of Invoice: 45 days from the date of invoice Amount of Invoice: ₹100,000.00 (Indian Rupee)

A). Payment made on 10-04-2025

1. Payments made within 45 days

2. Payments dated after end of the financial year

3. Payments are included in financial year 2024-2025

B) Payments made on 01-05-2025

1. Payments made outside of 45-day period

2. Payments made are not allowed in the financial year 2024-2025

3. Payments can only be claimed in the financial year 2025-2026.

Period of Interest for Delay in payment

If a buyer delays payment, the law requires them to pay interest at three times the RBI Bank Rate (as on year-end), compounded monthly.

The above interest will not be tax deductible under Section 80C of Income Tax Act.

Compliance Checklist for Businesses :

Businesses must act NOW to minimize their year-end disallowances.

6.1 Supplier Verification :

Collect Udyam Registration Certificates from your suppliers

Maintain a vendor master list containing your suppliers' MSME status

Update your vendor classification every six (6) months

Confirm all suppliers are Micro or Small (not Medium)

6.2 Agreements and Documentation :

Each of your MSME vendors must have a written agreement

Your Vendors payment term must be 45 days or less

There should be no verbal agreements (the default payment term is 15 days).

6.3 Automated Tracking System :

All vendors' invoice acceptance dates must be tracked

All the vendors' invoices must have a deadline of 15 days and 45 days

Set automatic reminders to send alerts 5–10 days before the due date.

Escalation alerts to be sent to your financial head

6.4 Review Periodically to Determine Tax Effect :

You must review your MSME vendors' outstanding balances on a monthly basis.

You must conduct a 43B(h) disallowance simulation.

You must have your final review of all your MSME vendors during the months of February and March.

6.5 Tax Audit Reporting - Form 3CD Clause 22 :

It is required that businesses must disclose the following:

Outstanding Principal Amount for MSME vendors

Outstanding Interest for MSME vendors

Total Breakdown of Micro and Small Amounts Due to MSME Vendors.

Common Risks of Non-Compliance

Have not established formal business agreements → 15 Day Credit will be forced to make payment.

Have not obtained an Udyam verification → Incorrectly classified under the wrong category.

Have not made payments within a single business day of receipt → Full year payment will be disallowed.

Year End cash flow stress → Delayed payments

Reporting incorrectly on Form 3CD → At-risk of an audit

Managing payments under the MSMEs' Act is no longer an option; it is now required by law.

Book My Accountant (BMA) is a specialist in the area of Vendor Management and MSME compliance w.r.t. 43B(h) advisory services, as well as tax audit documentation.

Within that scope, we provide the following services:

1. Udyam Certificates/Vendor Due Diligence

Obtaining valid Udyam Certificates.

Mapping to the MSME Status.

Updating vendor classifications as needed.

2. Agreements Drafted and Standardized

Legally compliant contracts – minimum of 45-day contracts.

Protection from a default within the minimum of 15-day rule.

Documentation following the requirements of the MSMED Act.

3. Automated Invoice Tracking

Real-time monitoring.

Alerts when due dates are approaching.

Dashboards showing invoices due for escalation.

4. Simulations of the 43B(h) at Year-End

Predicting potential disallowances for a subsequent tax year.

Identifying invoices which require immediate payment.

Avoiding the risk of unexpected tax liabilities.

5. Tax Audit/Form 3CD Reporting (Clause 22)

Providing accurate MSME disclosures.

Providing calculations of interest.

Providing audit support and representation to clients.

Tips for Business Owners :

Section 43B(h) is non-negotiable and strictly applied. You must pay within 15 or 45 days to claim the deduction; otherwise, the tax authorities will disallow the expense and add it to your taxable income. MSME interest cannot be deducted. The period from February to March could have the highest risk for business owners. Further, audit report preparation requires clean documentation.

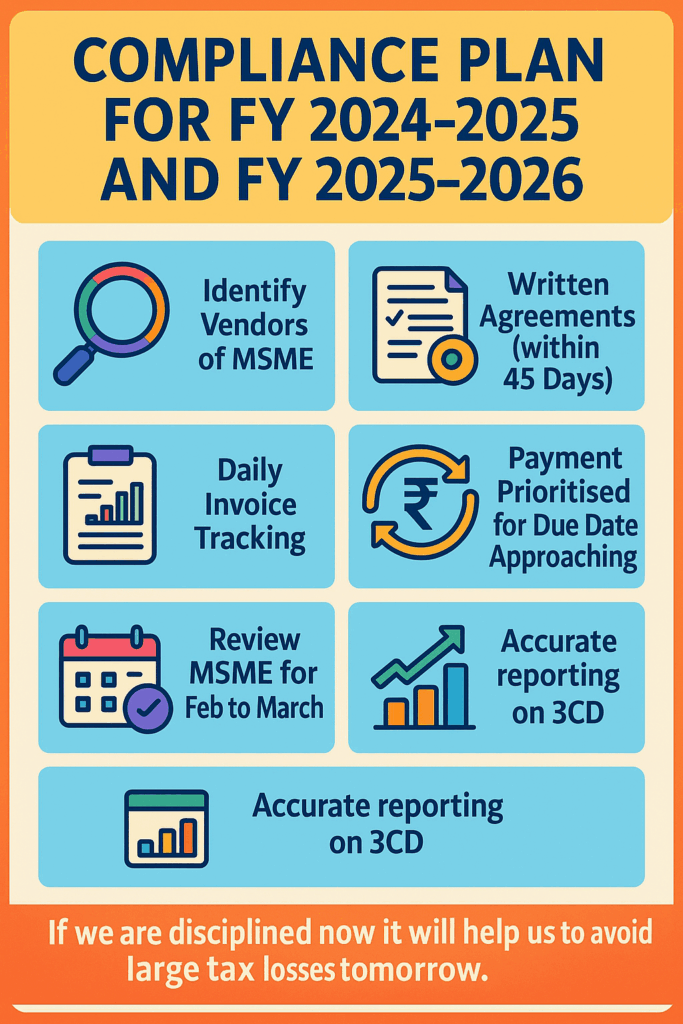

Compliance Plan For FY 2024-2025 And FY 2025-2026

Identify Vendors of MSME

Written Agreements (within 45 Days)

Vendor Master Updated

Daily Invoice Tracking

Payment Prioritised for Due Date Approaching

Review MSME for Feb to March

Accurate reporting on 3CD

If we stay disciplined now, we will avoid large tax losses in the future.

Disclaimer

This website is intended to provide information and education (in general) to the reader and should not be regarded as advice on any issue, including legal advice, tax advice, or compliance advice. Legal requirements, notifications and tax laws may change. Readers should seek professional advice from a qualified professional for a thorough understanding of their own situation or check the latest legal amendments on the government websites. Book My Accountant (BMA) provides professional services; however, this document's content is not intended to be a substitute for BMA's personal advisory services.

How to Prepare GSTR-9 & 9C: A Full Working Checklist for FY 2024-25

Filing GST annual return (GSTR-9) and reconciliation statement (GSTR-9C) always looks cumbersome for the financial year, as annual GST compliance may look tedious at times. Therefore, this guide will not only take you through that step-by-step process but will also provide a practical checklist of all of that and include links to official documentation for your ease of reference, so you can stay on top of compliance regulations.

In essence, this serves as the summary of your GST data, such as outward supplies, inward supplies, ITC claimed, reversals, tax paid, and adjustments, for the financial year, which is then presented in a consolidated GST return. You can find it covered in the manual of the portal.

GSTR-9C – Reconciliation Statement

This form is required when your aggregate turnover exceeds the limit of ₹ 5 crore (based on threshold limit, which is currently ₹ 5 crore) and you have to provide a reconciliation of your annual return with the audited financials.

Key bullets points:

Threshold of ₹ 5 crore aggregate turnover: notification number 30/2021 dated 30 July 2021.

Deadline for filing: Along with GSTR 9 (typically by 31 December in the following year).

Structured Step-by-Step Method for Completing GSTR-9

Step 1

Gather the Required Returns & Records

All monthly/quarterly returns: GSTR-1 (outward supply) and GSTR-3B (summary of tax)

Use the compute liabilities option on the portal in filing GSTR-9 (important step)

Preview your draft tax return done carefully, make sure to fix mismatches/faults

File using DSC/EVC if necessary

Keep your acknowledgment and proof of filing for your records.

Structured Step-by-Step Method for Completing GSTR-9C

When it is time to file GSTR-9C, here is the procedure to follow:

Step 1

Download Financial Statements : Audited P&L, Balance Sheet, and Trial Balance as well as the Annual accounts as per Companies Act, or audit requirement applicable for your entity.

Step 2

Turnover Reconciliation : Turnover based on books vs GSTR-1 vs GSTR-3B vs e-way bills (if applicable) and identifying differences and the reasons for each difference (for example, exports, exempt supplies, etc.)

Step 3

ITC Reconciliation : ITC based on books vs auto-data (GSTR-2B) and consider any blocked credits, reversals and RCM credit (if applicable) differences and provide a report or reason for any unreconciled differences

Step 4

Taxes Paid Reconciliation : Also, compare the tax liability shown in GSTR-9 with the actual tax payments, and adjust any pending or late-paid liability.

Step 5

Part-A for GSTR-9C (Reconciliation Statement) : In addition, Part A would include turnover, ITC, taxes paid, and any non-reconciled items, accompanied by the reasons for such differences.

Backup all data, take printout/screenshot for the client

Common Mistakes

Reporting turnover incorrectly (under/over)

Not accounting for ineligible ITC / not taking back

Not taking back RCM (reverse charge mechanism) liabilities

Not checking or reconciling Table 8 (ITC per portal) to books

Not filing or filing late (for GSTR-9C) and incurring excess penalty.

Why Choose BookMyAccountant for Your Filing?

Ifyou want a stress-free and accurate filing experience, consider Book My Accountant.

Qualified CA and GST experts with previous experience in filing annual return and completing reconciliations.

Full end-to-end service: Data reconciliation completed, auditing coordinated if applicable, and e-filing handled through the portal.

Transparency in pricing and non-googling every filing deadline (so we won't miss 31st December filing deadline).

Safeguard your books and any filings or data related to your GST.

Furthermore, you will be able to reach our client support team for any inquiries, even towards the end of your client experience.

Email or call us today and we will schedule your GST return review and you will never worry about GST compliance again, to be done professionally.

Disclaimer

This Blog provides information only and does not provide any professional tax or legal advice. Although we have made an effort to ensure the material is factually accurate as of the original date of publication, the GST legislation, rule and thresholds can change. Taxpayers should obtain updated provisions from the CBIC official portal, or enlist the services of a qualified tax professional. BookMyAccountant assumes no liability, and is not responsible for any errors or omissions in the information or for any actions taken by any party in reliance upon information contained in this Blog.

Upgrade Alert: 6 Key Changes to GST Invoice Management System (IMS) You Need to Know!

Say Goodbye to ITC Headaches! The New GST System is Coming in October 2025

A significant transition will occur in regard to how taxes are managed by Indian enterprises. The GST Invoice Management System (IMS) will undergo a development and mandatory migration beginning in October 2025, which represents a significant development and will enhance accuracy and transparency throughout the process. The IMS aims to create unmatched flexibility; moreover, it addresses critical business challenges, particularly with respect to Input Tax Credit (ITC) management and buyer-supplier reconciliation.

Here are the 5 crucial updates you must prepare for to ensure seamless GST compliance:

1. The Smarter “Pending” Option is Now Extended to Critical Documents

Previously, the GST portal’s ‘Accept’ or ‘Reject’ choices were too forgiving for businesses; for instance, they compelled you to make decisions hastily, potentially leading to incorrect outcomes. The upgrade to the IMS offers well-deserved flexibility in regards to actions on additional types of documents -

Credit Notes (CN)

Debit Notes (DN)

Invoices with amendments

Why it is important to your business: This additional feature provides comfort that you can mark something as Pending (CN) without having to make an irreversible decision in a hurry. Now you can take your time to mark the Credit Note as Pending until you verify the goods were returned and confirm whether you want to claim it or reverse the ITC.

2. Mandatory Remarks for Rejections or Pending Actions

A major pain point in GST reconciliation has always been the communication gap between buyers and suppliers. If a supplier either rejected or left an invoice or credit note pending, the supplier often had no idea why which initiated the long email threads, delayed adjustments of ITC and continuous back and forth phone calls.

The new IMS update (effective October 2025) is addressing this issue directly by making it mandatory for a recipient to provide remarks every time a recipient:

When you take one of these actions, you can provide a reason:

“Goods not received.”

“Wrong GSTIN / Party mismatch.”

“Wrong value or tax rate.”

“Duplicate invoice.”

“Awaiting credit note confirmation.”

“Goods returned and waiting for verification.”

Why This is Important for Businesses

Increased Transparency

Both parties know exactly why an invoice or note was rejected or left pending; there is no more guessing, and clarification no longer requires back-and-forth communication.

Faster Reconciliation

The suppliers can instantly correct or re-issue the document based on the visible remark, which reduces the dispute cycle from weeks to days.

Better Audit Trail

The remark constitutes part of the document history saved in the GST system, providing a digital trail to facilitate compliance review and audit workflows.

Reduced ITC Disputes

Buyers can rest assured knowing their Input Tax Credit (ITC) will be allowed or put on hold; the status, and reason or reasons are clearly documented on both sides.

Increased Professional Accountability

Because remarks are visible to both users, it facilitates a culture of accuracy, ownership, and problem-solving in every transaction.

3. Critical: New Rules Apply ONLY from October 2025 Onwards

It is very important to note that the new IMS features do not apply to prior transactions. Your organization will be working in a dual system for a period of time:

Document Type

Date of Document

System Rule Followed

New Regime

October 2025 or later

Pending option, partial ITC reversal, etc.

Old Regime

Before October 2025

Previous rules (no pending, mandatory full ITC reversal, etc.)

Be sure your accounting software and internal processes are immediately able to accommodate the simultaneous existence of both "old" regime documents and "new" regime documents. Your team must accurately identify the date prior to processing any document.

4. Deep Dive: Flexible ITC Reversal

Clarifying Flexible ITC Reversal – A More Intelligent, Proportionate Approach

Beginning October 2025, IMS goes live with Flexible ITC Reversal. This amendment closes the gap between a CN issuance and the recipient’s ITC claim, while promoting flexibility, accuracy, and fairness in GST compliance.

The Issue with the Previous System

In the previous GST regime (before Oct 2025), a recipient reversing a Credit Note had to reverse the entire ITC linked to that invoice, regardless of what ITC they had actually claimed.

Too much ITC has been reversed, manual reconciliation proves problematic, and buyers and sellers engage in unnecessary disputes.

Example:

A purchaser received an invoice with ₹18,000 GST, and, for various internal accounting reasons, had only claimed ₹10,000 initially. Then, the supplier issued a Credit Note for ₹9,000 GST.The original recipient would reverse ₹9,000 of qualified ITC, even though only half of it was applicable.

The New Flexible System (Post-October 2025)

With the updated IMS, taxpayers have the flexibility to choose a full or partial ITC reversal depending on their actual ITC claim.

When a Credit Note is issued and a reversal occurs, the IMS asks the recipient the following direct question:

"Do you want to reduce ITC for this record?"

Most likely, the next action will be as follows:

If yes, you are able to enter the exact amount of ITC amount and reduce it for that record - there will be no assumptions of any kind and no obligation of full reversal.

If no, the ITC will remain unchanged - until you choose to manually edit it at additional time (if at all).

This change gives businesses "control" to confirm that the ITC reversal is the same as what their real book entries are - not the assumptions of the ITC reversal from the system.

Feature

Old System (Pre-Oct 2025)

New System (Post-Oct 2025)

Compliance Impact

Reversal Amount

Full ITC reversal on original invoice/debit entry linked to Credit Note.

Partial or full reversal can be selected by the recipient.

Prevents over-reversal; aligns reversal with actual ITC claimed.

System Prompt

System assumed full reversal; manual correction required.

System prompts with “Do you want to reduce ITC for this record?”

No flexibility – automatic or full reversal expected.

‘Yes/No’ choice + editable reversal field.

Flexibility ensures book-level accuracy and smoother audits.

Example for Better Understanding

Let’s say:

Supplier issues an invoice for ₹1,00,000 + ₹18,000 GST.

The recipient claims ₹10,000 ITC initially due to an internal error; consequently, we must conduct further verification to reconcile the figure with supporting documentation.

Later, the supplier issues a Credit Note reducing the value by ₹50,000 plus ₹9,000 GST; thereafter, the adjustment should be reflected in the records and reconciled with supporting documentation.

Now:

Old System: The recipient would have to reverse the entire ₹9,000, even though only ₹10,000 ITC was ever claimed.

New System (Post-Oct 2025): The system asks whether the recipient wants to reverse ITC.

Recipient selects ‘Yes’ and enters ₹5,000 — half of their originally claimed ₹10,000 ITC.

This ensures perfect alignment between the supplier’s CN and the recipient’s ITC records.

5. New Table in Annual Return (GSTR-9) for Full Transparency

The GST Network (GSTN) has added a new table — Table 6A1 — in the Annual Return (Form GSTR-9) for FY 2025–26 onward for better clarity and accountability of Input Tax Credit (ITC) in one's GST return. The new table aims to give you a complete overview of your ITC movement throughout the financial year with complete transparency with your books, GSTR-3B, and GSTR-2B.

What Table 6A1 Captures

The new table has three relevant stages of your ITC life cycle:

Total ITC Claimed During the Year –

This is your claimed ITC in total in GSTR-3B for the financial year as at the end of the period. For example, if the claimed ITC of the year across return(s) comes out to be ₹5,00,000, the amount would appear here. Furthermore, you can verify the figure against your records, and if there is a discrepancy, you can initiate a reconciliation.

Total ITC Reversed Later –

The statement covers scenarios in which ITC was reversed for ineligibility: the recipient did not match the invoice, the vendor was not paid within 180 days, or reversal occurred for any other compliance reason.

For example, you claimed ₹5,00,000 but later reversed ₹50,000 for unmatched invoices.

Final Actual ITC Utilized –

This is the net ITC after reversals, which was eligible, and utilized against tax liability. Final actual ITC utilized = ₹4,50,000 (Claimed - Reversed [i.e., ₹5,00,000 - ₹50,000]).

Disclaimer:

The purpose of this blog is purely to make people aware and provide information. It is not tax or legal advice. Interpretation may differ and tax law can change. Always consult a professional tax advisor before making any tax or financial decision.

The New Income Tax Act of 2025: A Complete Guide for Taxpayers

A new era is going to dawn in India's tax regime. With effect from April 1, 2026, the Income-tax Act, 2025 will take effect in lieu of the Income-tax Act of 1961, which has been in force for more than 60 years. This is history's biggest tax reform, not another amendment.

The new Act is aimed at modernizing regulations, easing tax compliance, and keeping pace with India's digital economy. Everyone who is a taxpayer -- individuals, start-ups, businesses, or charitable trusts -- will be affected.

Whether you are a private taxpayer, business person, or professional responsible for the preparation of GST returns or electronic tax returns, we at Book My Accountant (BMA) are here to assist you through these changes.

The Need for a New Income Tax Act

After decades of revisions, the Income-tax Act of 1961 had grown too complicated and antiquated. It was challenging for professionals and taxpayers to understand, with over 800 sections and multiple clarifications.

Among the principal concerns were:

Too many layers and overlapping rules make up a complex structure.

Outdated clauses: Allusions to antiquated methods.

High litigation: Disputes and administrative hold-ups are common.

To address this, the government unveiled the Income-tax Act, 2025, which was designed from the ground up to give taxpayers a more straightforward, streamlined, and digitally-first system.

Main Features of the New Income Tax Law

With only around 536 sections compared to 800+, the new Act is significantly shorter. A few of the main reforms are as follows:

1. The concept of the tax year

The terms "Assessment Year" and "Previous Year" are no longer interchangeable. From now on, it's just Tax Year, which is less onerous to follow.

2. Digital-First Structure

The government has turned digital in its thinking with full-fledged online notices, time-bound refunds, and faceless assessments. All steps in the compliance process are supposed to be monitored online.

3. VDAs (Virtual Digital Assets)

Cryptocurrency, NFTs, and tokenized assets are defined and taxed for the first time. The unreported holdings can be considered as unaccounted income, and VDA gains are taxable.

4. Plain Words

Heavy legalese is not used in the Act. The language used in the provisions is simpler and more understandable, easy for common taxpayers to read and understand.

5. Notice Before Enforcement

Where there are no exceptional circumstances, advance notification has to be provided by the tax department before any action for enforcement, e.g., search or seizure. This renders the process even more equitable.

6. Charitable Institution and Trust Regulations

There will be exemptions only for valid charitable purposes. There are more stringent reporting requirements and disincentives for gifts anonymously made.

Individuals' New Tax Slabs

The Act now incorporates the new tax slabs announced in the Union Budget 2025. With effect from FY 2025–2026, the following apply:

Range of Incomes (₹)

Rate of Taxation

0–4,00,000

Zero

Between 4,00,001 and 8,00,000

5%

8,00,001–12,00,000

10%

12,00,001–16,00,000

15%

16,00,001–20,00,000

20%

Between 20,00,001 and 24,00,000

25%

Over 24,00,000

30%

Key Points to Note

The normal deduction was raised to 75,000.

Section 87A Rebate: Maximum ₹60,000, effectively tax-free income of ₹12 lakhs.

Default Regime: The taxpayers can choose to go under the old regime if they want; the new regime is the default instead.

Surcharge: Reasonable for high-income earners.

The plan here is to discourage the use of deductions and make it easier to file.

Reductions and Rewards:

The Act retains a few common deductions despite reducing exemptions:

Although the focus on the new regime is more now, 80C investments are still there.

Health insurance (80D): Continues with additional GST exemption.

80JJAA (New Employee Deduction): Provides an additional 30% deduction of salaries of fresh hires to promote employment generation.

MSMEs and start-ups: Continue to avail of relief in tax and simplified schemes.

For tax, the Unified Pension Scheme (UPS) is treated on par with the NPS.

Evaluations and Compliance:

The government is emphasizing faceless digital compliance. Some of the major changes include:

Faceless Assessments: We will handle all cases anonymously to avoid harassment.

3-Year Filing Limit: We cannot file returns after three years from the due date.

Refund Timelines: They disburse refunds earlier, with a levy of penalty for late filing.

Enlarged Search Powers: After searching, the authorities can make use of social media and electronic devices.

Even though these steps streamline the process, they also create privacy issues, with access being in digital format.

Business Provisions:

Corporate Tax Rates: 15% for new manufacturing facilities and 22% for domestic businesses

Start-ups: Clarity on angel tax matters, including VDA taxation.

International Investments: We continue to offer infrastructure exemptions to sovereign and pension funds.

Transfer Pricing: Streamlined with quicker decisions and anonymous resolution of disputes.

Non-profits and trusts

The new Act subject’s non-profit organizations to stricter treatment:

Anonymous donations are excluded.

Donations from corpus must be traced out and handled appropriately.

Expense on CSR is not allowable yet, but reporting must be simplified.

This only makes sure that legitimate non-profits are benefiting from tax relief.

Transition Rules

FY 2025–2026 (AY 2026–2027) will be governed by the 1961 Act.

New Act will come into operation fully on 1 April 2026.

Until they are overtaken, current regulation and case law will continue to inform interpretation.

Tax payers and companies ought to update their data, software, and planning techniques well in advance.

Practical Consequences for Individuals

Particularly in the default regime, return is simpler.

The old regime may still be the choice of major investors in tax-saving products.

When dealing with Companies

Accuracy is desirable but compliance is quicker and simpler.

With increased transparency, there is reduced scope for manipulation.

For tax planners and certified accountants

Both Acts need to be known side by side during the transition period.

Educating the client will be crucial in preventing misconceptions.

Pros and Cons:

Pros

Problems

1. Cleaner, modernized drafting. 2. Simpler abridged sections and slabs. 3. Faster refunds and fairer procedures. 4. Clear rules for digital assets and start-ups.

1. Privacy issues with increased digital access. 2. High-deduction taxpayers (housing loan, PF, LIC) might feel penalized. 3. Enterprises making the transition will have to adjust quickly.

Conclusion

India's tax system has completely changed as a result of the Income-tax Act of 2025. It seeks to align with India's digital economy while making income tax easier, quicker, and more equitable.

For individuals, it means filing tax returns will be less complicated. It represents a shift for companies toward efficient, transparent, and faceless compliance. It's also time for professionals to help clients make the change.

Our goal at Book My Accountant (BMA) is to make this transition as smooth as possible. Our professionals can assist you in meeting your ITR filing deadline, staying in compliance with the new tax regime, and streamlining electronic income tax filing so you can concentrate on what really counts: expansion.

Disclaimer:

The purpose of this blog is purely to make people aware and provide information. It is not tax or legal advice. Interpretation may differ and tax law can change. Always consult a professional tax advisor before making any tax or financial decision.

Waiver of TDS/TCS Interest Under Sections 201(1A) (ii) and 206C (7): CBDT’s 2025 Relief

A significant tax relief has been announced by the Central Board of Direct Taxes (CBDT). For qualified cases, CBDT waives the interest levy under Sections 201(1A) (ii) and 206C(7) of the Income-tax Act through its 2025 circular no. 08/2025.

The goal of this action is to lessen the financial burden of taxpayers who had to pay interest on TDS/TCS payments that were delayed for valid reasons. This relief is a much-needed reprieve for a lot of people and businesses.

However, what is the true meaning of this waiver? And who stands to gain from it? Let's dissect it.

What Is This Waiver About?

Interest on late or non-payment of TDS (Tax Deducted at Source) and TCS (Tax Collected at Source) is covered by Sections 201(1A) (ii) and 206C (7) of the Income-tax Act.

In the past, taxpayers were still required to pay interest even if the delay was caused by technical difficulties or banking problems.

The CBDT declared in 2025 that in worthy cases, such interest may now be waived. Following comments from taxpayers and industry experts, this decision is described in detail in Circular No. 08/2025.

Why Did CBDT Announce This Relief?

The government's goal to facilitate compliance and assist legitimate taxpayers is reflected in the waiver.

Numerous companies, particularly start-ups and MSMEs, stated that the following factors frequently caused TDS/TCS deposit delays:

Technical issues with banking systems.

Payment is started ahead of schedule, but credit is given after the deadline.

Errors in the processing of payments even though taxpayers took prompt action.

The CBDT recognizes these practical difficulties and guarantees that no taxpayer is unjustly punished by permitting a waiver.

Who Is Eligible for the Waiver?

Not everybody is eligible. The recipients of this relief are taxpayers who actually experienced hardship.

Eligible cases include:

1. Payments made in advance of the due date but credited later because of system problems are examples of eligible cases.

2. Unintended delays that are out of the taxpayer's control.

3. situations in which taxes were paid but interest was assessed.

Ineligible cases:

1. Intentional non-payment or wilful defaults.

2. Persistent late filers without good cause.

Applications must be sent to the appropriate authorities, such as the Director General of Income Tax (DGIT), the Principal Chief Commissioner of Income Tax (Pr. CCIT), or the Chief Commissioner of Income Tax (CCIT).

The deadline for applying

A stringent deadline has been set by the CBDT.

Within a year of the fiscal year in which the interest was assessed, taxpayers must submit an application.

As an illustration:

The application needs to be filed by March 31, 2025, if interest was assessed in FY 2023–2024.

Since this deadline cannot be negotiated, prompt action is essential.

Why This Is Important for New Businesses and Start-ups:

Every rupee matters for new and start-up companies. Even minor fines are a major hardship due to tight budgets, scarce financial resources, and ongoing pressure to fulfil compliance requirements. This is particularly true for MSMEs, who sometimes lack specialized compliance teams and find it difficult to stay on top of constantly evolving tax laws.

The respite is especially helpful for STPI-registered corporations and IT firms that specialize in exports, as international banking procedures and transactions can occasionally result in unanticipated delays in TDS/TCS payments. These companies, who are already dealing with a number of operational difficulties, now have a safeguard against unjust interest charges brought on by uncontrollable circumstances.

We at Book My Accountant (BMA) collaborate closely with IT companies, MSMEs, and start-ups to assist them understand and comply with complicated tax laws. More than merely monetary comfort, this waiver gives these companies the chance to refocus their efforts on expansion and innovation rather than worrying about fines for inevitable delays.

How to Apply for the Waiver?

Here is a basic guide:

Examine your TDS/TCS transactions.

Verify whether interest has been assessed under Sections 206C(7) or 201(1A)(ii).

Gather supporting documentation.

Collect proof of payment initiation, bank statements, and any correspondence pointing out technical difficulties.

Create an application draft.

Request a waiver and provide a clear explanation of the delay.

Send to the appropriate authority

Send it to DGIT, CCIT, or Pr. CCIT by the deadline.

Follow-up

Keep track of your application and answer any questions the department may have.

What Effect Does This Have on You?

You now have the opportunity to get relief if you have paid interest or been charged interest as a result of actual banking or system errors.

For businesses, this means:

Improved cash flow since excessive interest is no longer a burden.

Increased confidence in compliance as a result of knowing that honest mistakes are handled fairly.

Why BMA Suggests Quick Action

Book My Accountant (BMA) has witnessed personally how quickly important deadlines can pass when tax compliance isn't given first priority. Therefore, if you think you are eligible for this waiver, we strongly advise you to take immediate action. Early application submission lowers last-minute stress and improves your chances of approval. Seeking professional aid is equally vital because applications that are accompanied by well-organized documentation have a much higher chance of being accepted. In order to ensure future operations, go more smoothly, now is also a great time to assess and enhance your TDS/TCS compliance procedure.

Popular Takeaways:

A significant 2025 relief is the CBDT's waiver of the interest levy under Sections 201(1A) (ii) and 206C (7).

Applications must be made on time.

Exporters, MSMEs, and startups stand to gain a great deal.

You can increase your chances of approval by seeking professional advice.

Conclusion:

Sections 201(1A) (ii) and 206C (7) of the CBDT provide a 2025 interest waiver, which is a welcome relief for upfront taxpayers, particularly exporters, MSMEs, and start-ups that are facing inevitable delays. It shows that the government wants to make compliance more equitable and useful. But because the relief is application-based and subject to stringent deadlines, prompt action is crucial.

To increase their chances of receiving this benefit, Book My Accountant (BMA) assists individuals and companies in creating strong applications with the required supporting documents. Now is the time to take action and lessen needless financial burden if you think you qualify.

Disclaimer:

This article has been prepared by Book My Accountant (BMA) for general awareness purposes. It is based on publicly available information and CBDT circulars. It should not be treated as legal or financial advice. For personalized consultation, please connect with a qualified tax expert.

Mandatory ISD Registration from 1st April 2025

Mandatory registration as an Input Service Distributor (ISD) is required for all entities that have more than one GSTIN based on a single PAN effective 1st April 2025. ISD registration was previously optional, but it is now mandatory as per the new GST amendment. This amendment aims to facilitate the distribution of Input Tax Credit (ITC) while ensuring compliance and allowing credit management for entities with multiple branches. Companies receiving standard input service bills at a head office and distributing ITC to multiple branches will be most affected. To comply, they must pre-register as ISDs, establish proper ITC distribution processes, and ensure effective compliance practices from the start.

Understanding Input Service Distributor (ISD)

An input service distributor is an office of the business that receives tax invoices for input services and distributes the available input tax credit (ITC) to related branches or units having separate GSTINs but using the PAN of that business. Distributing Input Tax Credit The input tax credit (ITC) available for distribution in every month has to be distributed in that month itself and to be reported in Form GSTR-6. Furthermore, the ISD must distribute every tax credit arising from payments made under the reverse charge mechanism under Sections 9(3) and 9(4) to the respective recipients. If the input service is availed only by one recipient, input tax credit should be distributed to that one recipient only. To distribute the available tax credit among multiple recipients who use the input services, they must do so in proportion to their turnover.

The distribution has to be done, ITC to Branch = (Branch Turnover / Total Turnover) x Total ITC Branch Turnover = turnover, as referred to in section 20, of person R1 during the relevant period Total Turnover = the aggregate of the turnover, during the relevant period, of all recipients to whom the input service is attributable in accordance with the provisions of section 20 Total ITC = the amount of credit to be distributed. XYZ Ltd. is a company with its head office in Mumbai (ISD) and branch offices in Delhi, Bangalore, and Chennai. The Mumbai head office receives an invoice from an advertising agency for ₹1,00,000 + 18% GST (₹18,000 GST Credit). This advertisement benefits all three branches, so the ITC needs to be distributed proportionately.

Turnover of Branches:

Delhi Branch: ₹10,00,000

Bangalore Branch: ₹5,00,000

Chennai Branch: ₹5,00,000

Total Turnover = ₹10L + ₹5L + ₹5L = ₹20,00,000

ITC Distribution Calculation:

Since the ITC of ₹18,000 needs to be distributed based on turnover, the allocation is:

Branch

Turnover (₹)

Share (%)

ITC Distributed (₹)

Delhi

10,00,000

50%

₹9,000

Bangalore

5,00,000

25%

₹4,500

Chennai

5,00,000

25%

₹4,500

Total

20,00,000

100%

₹18,000

Financial Risks of Non-Compliance with ISD Rules-

Failure to comply with Input Service Distributor (ISD) rules poses significant financial and operational risks to business organizations. Non-compliance with ISD protocols would deny branches any allowable Input Tax Credit (ITC) for general services, which would only increase tax cost. Similarly, errors in ISD and/or mismatches of ITC in Goods and Services Tax (GST) returns would increase the likelihood of receiving a GST notice, or auditing, and/or potential penalties.

Non-compliant businesses face increased scrutiny from tax authorities due to uncertainty in ITC apportionment, raising the risk of financial liabilities. The cost of ITC would be much more significant if taxpayers could claim benefits for any Reverse Charge Mechanism (RCM) transactions prior to April 2025, which leads to additional taxes being paid. However, this holds true if the company ensures satisfactory ISD compliance, properly apportions the ITC between branches, reduces compliance risks, and results in lower taxes with a clear flow of ITC. It also supports claiming ITC based on RCM, subsequently after April 2025, improving cash flow for the company's overall improved tax efficiency. To reduce tax litigation and financial losses, companies must value their ISD compliance and ensure proper ITC disbursement.

Conditions to be Met by an Input Service Distributor (ISD)

Registration:

An Input Service Distributor (ISD) is required to separately register as an "ISD" in addition to their regular GST registration. When applying through REG-01, the taxpayer will have to indicate ISD registration at serial number 14. Under the law, only upon making that declaration is the ISD permitted to distribute Input Tax Credit (ITC) to its recipients.

Invoicing :

Raise ISD invoices while disbursing ITC to respective units or branches.

Filingof Returns:

The returns will be filed on a monthly basis in GSTR-6 on or before the 13th of the ensuing month reporting the ITC paid out.

Returns:

The total tax credit paid out by the aggregators should not exceed the available tax credit at the end of the relevant month.

Filling :

ISD has to report the remitted ITC in GSTR-6, to be filed by 13th of next month.

Consequences of Not Registering as an Input Service Distributor (ISD)

From April 1, 2025, companies that do not register as an Input Service Distributor (ISD) can encounter various difficulties, including legal and monetary penalties:

Penalties and Interest

Failure to comply with obligatory ISD registration can invite penalties for improper distribution of Input Tax Credit (ITC). If ITC is claimed in excess, tax officials can recover it from the recipient along with interest under Section 21 of the GST Act.

Increased GST Audits and Scrutiny

Companies that are not registered under ISD are prone to audits and investigation by the tax department. Discrepancies in the claim of ITC can invoke in-depth inquiry, resulting in legal issues.

ITC Reversal and Cash Flow Interruptions

Incorrect or non-registered ISD operations might lead to ITC claim reversal. This makes branches pay tax directly rather than availing eligible ITC, affecting cash flow and working capital management.

Tax Notices and Financial Burdens

Mistaken ITC claims at the head office without ISD registration can result in tax notices. These notices can translate into extra financial burdens and operational interruptions.

Operational Inefficiencies and Credit Allocation Problems

In the absence of an appropriate ISD mechanism, companies might find it difficult to distribute ITC effectively among various branches. This can lead to credit distribution disputes and financial management inefficiencies.

The entity must obtain a separate registration as an ISD, even if it has a normal GST registration.

Step-by-Step ISD Registration Process

Step 1: Access the GST Portal

Step 2: Navigate to Registration Application

Step 3: Fill Part A of Form GST REG-01

Step 4: Fill Part B of Form GST REG-01 Details of Promoters/Partners: Authorized Signatory: Bank Account Information

Step 5: Upload Required Documents a. Proof of Constitution of Business b. Proof of Principal Place of Business c. Identity and Address Proofs of Promoters/Partners d. Bank Account-Related Proof e. Photograph of Promoters/Partners f. Letter of Authorized Signatory in case of partnership firm, company, HUF, etc. g. DSC in applicable cases like company , etc.

CONCLUSION

We at BMA take satisfaction in streamlining tricky tax regimes, and if each person is best proper to showcase this, it's far the Input Service Distributor (ISD) device beneath GST. Compliance calls for a painstaking recognition on detail, consistency, and a clear information of the way to distribute enter tax credit (ITC) between divisions. That's wherein we step in. We provide full support for businesses with ISD registration, compliance setup, and monthly return filings. Our strong approaches ensure that we assign ITC appropriately and fairly at locations, preventing mistakes, loss of credit, and undue notices from the tax department. Whether you have a decentralized headquarters or are a large company with decentralized operations, we streamline ISD management to ensure your tax credits are compliant and optimized.

With us on your side through BMA , you can cast off tax monitoring issues and cognizance at the boom of your enterprise, as we deal with your ISD requirements with accuracy and on time.

Disclaimer

The above is general information. Material on this site is for general information purposes only. Readers are advised to consult a professional tax consultant before making any tax decision. Despite the exercise of care in updating information, BMA cannot be held liable for error or omission or loss arising from use of such information

AI for Tax Compliance : How It's Revolutionizing TDS Assessments in India

India's tax regime is undergoing a sea change with the introduction of Artificial Intelligence (AI) and Data Analytics. Tax Deducted at Source (TDS) evaluations, which previously had been based on human instincts, are now being managed by AI-powered automation and data analytics. It increases compliance, accuracy, and efficiency in calculating taxes, and business houses and chartered accountants are being forced to adopt such newer technology.

The Application of AI in TDS Evaluations

Artificial intelligence-based systems are transforming TDS evaluation services through automated procedures, identification of discrepancies, and reduction of errors. Earlier, manual reconciliation and data entry used to be performed, hence resulting in errors and inaccuracy in computation. AI-based platforms apply machine learning algorithms to reconcile transactions, enable accurate deductions, and meet government policies.

Key Advantages of AI in TDS Evaluations

Error Minimization: AI minimizes human error to a large degree by cross-verification with pre-defined taxation laws and prior experience.

Enhanced Processing: Computer-based processing minimizes processing time to a large degree compared to manual assessments.

Forensic Predictive: AI anticipates potential discrepancies in TDS filing so that business houses can solve the same in good time.

Compliance with Regulator Regulations: AI products reflect the newest tax laws, thus accurate deductions based on regulation changes.

Light heartedness to Enterprises for Engagement Adoption:

Use of AI for TDS auditing lightens the level of compliance attainable by companies without being bogged down by cumbersome weights of manual checks and adjustments.

Data analytics is especially applicable to enhancing TDS consultancy service by authenticating patterns, detecting possible frauds, and delivering tax deduction insights. In the era of generating vast amounts of financial information on a daily basis, sophisticated analytics solutions allow organizations to:

Set Deduction Patterns: Pattern recognition ability enables organizations to find maximum tax-saving possibilities.

Detect Frauds: Artificial Intelligence-based analytics recognize discrepancies in deductions, which are advantageous for tax consultants and auditors to correct the mismatches.

Enhance Decision-Making: Real-time data analytics allow tax experts to make an optimum decision on tax compliance and tax planning.

AI & Data Analytics in TDS Consultancy Services

Indian TDS consulting companies are further investigating the potential of AI and analytics in an attempt to deliver successful tax solutions to clients. Tax consultants are using AI-driven dashboards to evaluate tax liability, identify mismatches, and maintain legal compliances.

Book My Accountant, a leading tax and financial services brand, is at the forefront of this transformation. With its expertise in TDS assessment services, the company provides AI-driven solutions that simplify calculating and adhering to taxes.

Why Companies Need AI-Based TDS Consultancy Services

Firms in Bhubaneshwar, Kolkata, and Bangalore need professional consultancy in tax to handle the complicated TDS provisions. A professionally managed TDS consultancy firm Kolkata like Book My Accountant keeps firms up to date about changing tax laws without any interference of any human being.

In the same way, TDS consultancy Bhubaneshwar services also utilize AI-based analytics to assist in maximizing tax deductions and avoiding compliance problems. With the integration of AI, companies can automate repetitive tax activities, minimizing human intervention and enhancing accuracy.

For Bangalore companies, AI-based TDS consultancy Bangalore solutions make it an easy job to deal with taxes. From e-billing to auto-filing of tax, AI revolutionizes the process of how companies deal with TDS assessments.

How Book My Accountant Leverages AI & Data Analytics for TDS Compliance

Book My Accountant leverages AI solutions to provide easy TDS assessment services. The organization provides:

Automated TDS Filings: Quick processing and timely compliance.

Real-Time Tax Tracking: Real-time tax assessments through AI-based dashboards.

Tax Solutions Personalized: Customized solutions for maximizing tax deductions to the extent and penalties avoided.

Data-Driven Decision Making: Analytics-based to achieve increased accuracy and compliance with laws.

Deploying AI to TDS estimates is not the tomorrow dream but the reality for companies eager to match the pace with times in an age of tax automation.

Upcoming AI & Data Analytics Trends for TDS Assessments

The future of TDS computations in India will see increased developments in AI and analytics, including:

Blockchain Integration: Transparent and secure tax transactions.

Cloud Solutions for TDS: Remote management and auto-launch tax data.

Since there is going to be more advancement in AI, organizations employing AI-founded tax consultants are going to have quicker, bug-free, and compliant TDS calculations.

Conclusion

Artificial intelligence and data analytics are revolutionizing tax deduction at source assessment services and making it fast, efficient as well as accurate. Book My Accountant offers industry-best TDS consultancy services in Bhubaneshwar, Kolkata, and Bangalore for implementing AI-based solutions for authentic taxes.

To experience the best-in-class AI-based TDS solutions, schedule an appointment with Book My Accountant today and enjoy a hassle-free experience of technology at tax.

Disclaimer

The above is general information. Material on this site is for general information purposes only. Readers are advised to consult a professional tax consultant before making any tax decision. Despite the exercise of care in updating information, Book My Accountant cannot be held liable for error or omission or loss arising from use of such information.

Major Income Tax Modifications for FY 2025-26: NIL Tax on Incomes up to Rs 12 Lakhs

Revised Tax Slabs

The budget introduces a restructured tax slab system to ensure a progressive taxation approach. The new tax rates are as follows:

New Income Tax Slabs for FY 2025-26 (as per Budget 2025)

Annual Income (₹)

Tax Rate (%)

Up to ₹4,00,000

No Tax

₹4,00,001 - ₹7,50,000

5%

₹7,50,001 - ₹12,00,000

10%

₹12,00,001 - ₹15,00,000

15%

₹15,00,001 - ₹20,00,000

20%

₹20,00,001 - ₹25,00,000

25%

Above ₹25,00,000

30%

This restructuring aims to provide relief to middle-income earners while ensuring that higher-income individuals contribute a fair share to the nation's revenue.

The Finance Minister's recent budget speech for the year 2025-26 has brought a revolutionary change in India's income tax scenario. This move is proposing people a great deal, especially those with an income of up to Rs 12 lakhs. In this blog, we shall introduce the main features and implications of the new income tax regime.

1. Exemption Limit: A New Beginning

Traditionally, the income tax exemption limit was Rs 2.5 lakhs for those who were less than 60 years old. In the following financial year, though, there was a surprise twist with those having income up to Rs 12 lakhs exempted from income tax. That is way higher than previous exemptions, and the idea is to lower tax on mid-level income earners.

2. Section 87A Extended Rebate

Most relevant among these extensions is the rebate under Section 87A for taxable incomes that have been lifted to Rs 12 lakhs. That is, such eligible assessee shall not only benefit from a bigger exemption limit but also from the rebate path. It must especially be noted in this regard that this rebate remains reserved only for resident individuals. Foreigners living in India or non-resident Indians are not eligible to claim it.

3. Tax Liability of Salaried Individuals

For salaried people, it is all the more useful. Although the minimum exemption amount is the same at Rs 4 lakhs, one can see that such people can be exempt from taxation up to a point of income of Rs 12.75 lakhs if one takes average deductions and other deductions into consideration. This brings the tax scenario for the salaried community more favourable, and they get to experience prosperity in terms of finance and consumption.

4. Special Rate Incomes: Clarification Needed

Though the new regulations have been welcomed with open arms, special rate incomes like Short-Term Capital Gains (STCG) have instilled fear.

These revenues are not liable for the rebate under the current clauses whether the aggregate revenue of the taxpayer is below Rs 12 lakhs. This provision of the new scheme has brought some ambiguity. Most of the taxpayers are enquiring whether they can avail themselves of the rebate scheme if their taxable revenue is mainly from such special sources.

5. Introduction of Marginal Relief

In order to avoid that the taxpayers suddenly find themselves bearing the tax burden as their incomes just cross Rs 12 lakhs, marginal relief has been provided for by the budget.

This is invoked when the taxpayer's income just crosses this threshold. The marginal relief provides that the tax levied on the income in excess of Rs 12 lakhs is never greater than the size of the excess income, in order to avoid so-called "tax trap." For example, a taxpayer can avail of a marginal relief of overall income of Rs 12,70,587, so that his total tax burden would be the size of the income in excess of Rs 12 lakhs.

6. Implications for the Taxpayer